Introduction

In today’s fast-paced digital era, instant payday loans online/tools/payday-loan-calculator promise quick cash, lightning-fast approvals, and easy access for individuals facing financial emergencies. But beneath the convenience lies a world of sky-high interest rates, debt traps, and regulatory scrutiny. This article explores 7 powerful truths about these loans—what they truly cost, why they remain controversial in 2025, where they are still legal, and how borrowers can make safer choices.

1. Eye‑Watering Interest Rates—Reality, Not Hype

Instant payday loans are synonymous with soaring APRs. Typical rates range from 400% to over 1,000% APR, depending on state and lender type enrichest.com+7Federal Trade Commission+7mirrorreview.com+7. In Texas, where regulations are very lax, borrowers frequently face APRs exceeding 500%, with average fees totaling $1.3 billion statewide in 2022 alone NCSL+5Houston Chronicle+5Federal Reserve+5.

These rates aren’t arbitrary—they stem from legal exemptions and weak usury caps in various states, allowing payday lenders to charge exorbitant fees for short-term cash advances Houston Chronicle+1Investopedia+1.

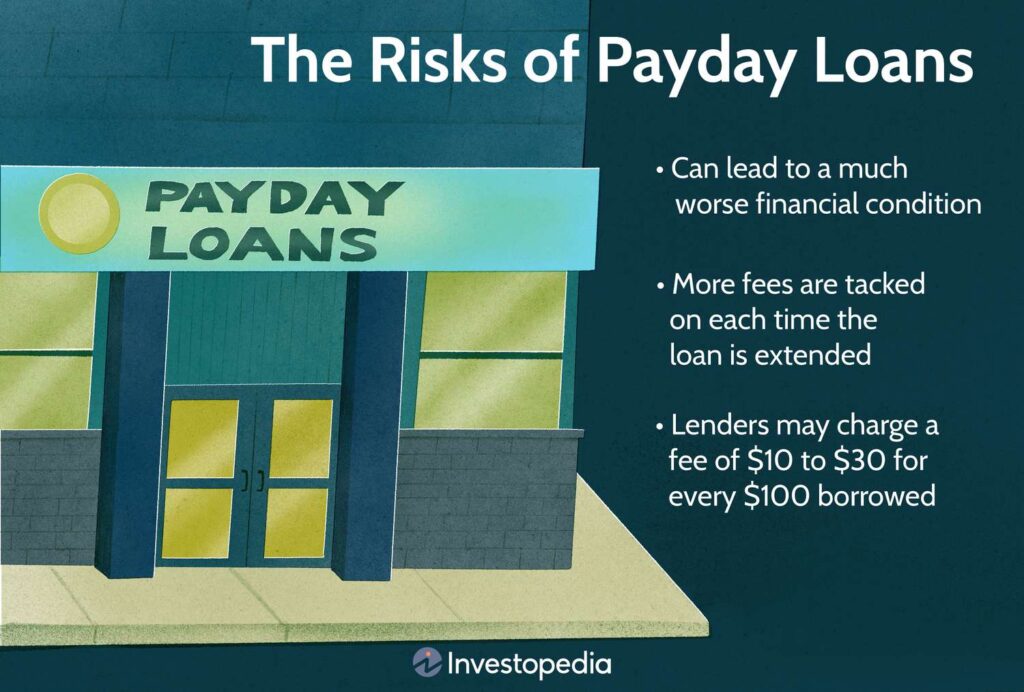

2. Short‑Term Loans Fuel Repeated Borrowing & Debt Cycles

Instant payday loans are meant to be repaid within two to four weeks. Yet when borrowers can’t repay on time, they often roll over or reborrow, incurring more fees each time. This is the classic payday debt trap—borrowers take multiple loans just to manage the fees from the previous ones Reddit+3enrichest.com+3Houston Chronicle+3.

According to Pew Trusts and other consumer advocates, many borrowers end up in debt more than half the year—often paying eight times the original loan cost in fees over repeated cycles pewtrusts.org.

Table of Contents

3. Huge Regulatory Divide: Legality Varies by State

In some U.S. states, payday loans are banned or heavily restricted. Laws in nearly 18 states plus Washington D.C. outlaw payday lending by capping APR rates at 36% or lower, effectively driving payday lenders out of the market Wikipedia+1Federal Reserve+1.

However, in states like Texas or Delaware, payday lending remains legal with minimal caps—leading to some of the highest APRs in the country (often exceeding 500–600%) Reuters+13Houston Chronicle+13Reddit+13.

4. Instant Online Access Masks Hidden Costs

“Instant” payday loans online may sound helpful—but many platforms charge origination fees, electronic withdrawal penalties, and even encourage ambiguous “tip” structures. In fintech variants like EWA (Earned Wage Access) platforms such as DailyPay or MoneyLion, small fees—when annualized—also equate to APRs of 200% to 750% Wikipedia+2Reuters+2AP News+2.

This type of credit, while fast, can still mask extreme borrowing costs beneath friendly branding GlobeNewswireAP News.

5. AI & Fintech: Better when Applied Ethically

The payday lending industry is increasingly using AI and machine learning for underwriting and risk modeling. This allows some lenders to approve borrowers without traditional credit scores, using alternative data like bank transaction history or employment patterns TachyLoans+1mirrorreview.com+1.

While this can increase access for underbanked consumers, it also heightens the risk of over-approval, opaque pricing, and continued exploitation when not accompanied by strong regulation.

6. CFPB & Federal Oversight vs. Legal Gaps

Though the Consumer Financial Protection Bureau (CFPB) regulates payday lending, its power is often limited by state-level variations. A 2025 Supreme Court ruling reaffirmed the CFPB’s authority—ensuring continued enforcement—but federal rules around underwriting and interest caps have been weakened since 2020 The Wall Street JournalInvestopediaFederal Trade CommissionInvestopedia.

For military borrowers, the Military Lending Act caps APR at 36%, regardless of state law, but most users of instant payday loans are civilian and ineligible for this protection Wikipedia+1Investopedia+1.

7. Better, Safer Alternatives Exist—but Awareness Is Low

Many financial experts and consumer advocates suggest alternatives:

- Earned Wage Access (EWA): Offers early access to pay with modest flat fees rather than interest—but even these fees can equate to high APRs and may cause dependency The Wall Street Journal+11AP News+11washingtonpost.com+11.

- Community Credit Unions & Small Personal Loans: Often offer much lower APRs, longer repayment terms, and flexibility.

- Emergency savings apps, small installment loans, or credit counseling can help individuals break the payday debt cycle GlobeNewswire+1pewtrusts.org+1Wikipedia+2Investopedia+2washingtonpost.com+2.

✅ Summary Table of 7 Key Truths

| Truth | Summary |

|---|---|

| 1. Sky‑high APRs | Typical 400–1,000% APR makes repayment difficult |

| 2. Debt traps | Rollovers and repeat loans deeply increase costs |

| 3. Legal patchwork | Some states ban, others permit with lax regulation |

| 4. Hidden charges | Tips, app fees, withdrawals obscure true cost |

| 5. AI underwriting | Expands access but may lack transparency |

| 6. Limited oversight | Federal rules exist, but enforcement is inconsistent |

| 7. Alternatives available | Safer credit sources exist; consumer awareness is key |

Voices from Real Borrowers & Trends

“High cost … annual interest rates of 400% or more … debt cycle” — common concerns shared on Reddit forums discussing payday loans Wikipedia+6Houston Chronicle+6Reddit+6Reuters+4Reddit+4Wikipedia+4Federal Reserve+2Investopedia+2Wikipedia+2Wikipedia.

The Washington Post warns financial predators—like payday lenders—operate ruthlessly, especially where consumer protection has weakened washingtonpost.com.

Meanwhile, the total market size for payday lending online continues to grow: expected to reach $37.5 billion by 2025, with digital platforms replacing storefront storefronts in many regions mirrorreview.com.

Practical Advice & Safer Actions

🧠 Think Twice Before Taking Out an Instant Payday Loan

- Check your state’s payday loan laws—many states cap APR or prohibit these loans entirely enrichest.com.

- Calculate true APR and total repayment cost—a loan of $500 at 400% APR repaid in 30 days costs nearly $750 GlobeNewswire.

- Avoid rollover fees—each rollover compounds debt rapidly.

- Consider alternatives:

- Community bank or credit union installment loan

- Borrowing from friends/family

- Earned wage access with low fixed fees

- Emergency budgeting tools or credit counseling

- Build an emergency savings buffer to avoid needing high-cost credit in the future.

Why This Topic Is Trending in 2025

- Increased visibility of fintech platforms, including EWA apps and online payday lenders, now servicing millions with just a smartphone download.

- Regulatory crackdowns and lawsuits, such as the 2025 New York lawsuits against DailyPay and MoneyLion, are drawing attention to exploitative APR models (200–750%) WikipediaReuters.

- Consumer education campaigns and nonprofit advocacy—like Pew Trusts—are pushing for stronger reforms, including meaningful interest caps and debt escape mechanisms pewtrusts.org.

Conclusion: Smart Borrowers Know the Truth

With “7 Powerful Truths About Instant Payday Loans Online That Every Smart Borrower Should Know”, you now have a grounded, nuanced view of this controversial product. While instant payday loans offer undeniable convenience, they come at a steep cost—and for many borrowers, that cost is crippling.

If after reading this you’re considering an instant payday loan, make sure you fully understand:

- The full APR, fees, and repayment timeline

- Your state’s legal protections or lack thereof

- Safer alternatives available to protect your finances